Morgan Stanley Identifies The Source Of Massive Treasury Selling

不同地理时区,最主要的是在欧洲和美国,在那里经常会出现有两个制度之间的公平“情绪”的差异:一个结束时,欧洲关闭和另一个起点,既有通常镜像。

但是,尽管我们主要关注地域对股市的影响,但摩根士丹利首席利率策略师马修·霍恩巴赫(Matthew Hornbach)在本周进行了更为有趣的观察,他在上周末确定了长期国债卖方的来源,即使不是完全相同的身份。在过去的几个月中,他不仅在美国利率空间,而且在股票和其他核心资产上引发了如此猛烈的溃败。

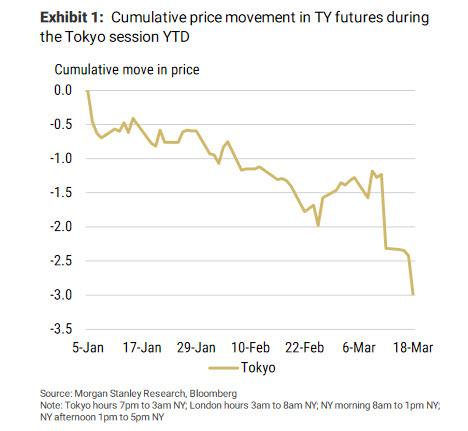

霍恩巴赫(Hornbach)的以下出色图表非常清楚地表明,美国国债期货的累积下行价格走势一直集中在东京交易时段。此外,在3月的第一周短暂休整之后,在FOMC会议之前,东京市场的卖盘急剧加速,此后持续。

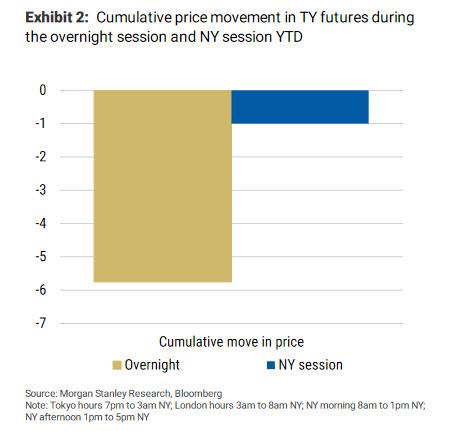

Of course, the initial burst of Treasury futures selling - which appears to have originated out of Japan every time - would then have a domino effect on the rest of the world, and as Morgan Stanley notes, "weak price action during the Tokyo session led to additional selling during the London session" although to a lesser extent. As the next chart shows, since the start of the year, 85% of the cumulative decline in TY futures prices occurred in the overnight session, i.e., Japan is almost single-handedly responsible for the dump surge in yields this year!

Why does this matter?

Because if Morgan Stanley is right, and if the seemingly daily Treasury selling indeed originates out of Tokyo, there is finally good news for bond bulls: Hornbach writes that "we have good reason to believe the selling from Japan won't last... into April." That's because the fiscal year in Japan ends on March 31. "At that point, liquidation of non-yen bond holdings should stop, if not reverse at some point in the April-June quarter."

But why did Japan sell non-yen bonds in the first place?

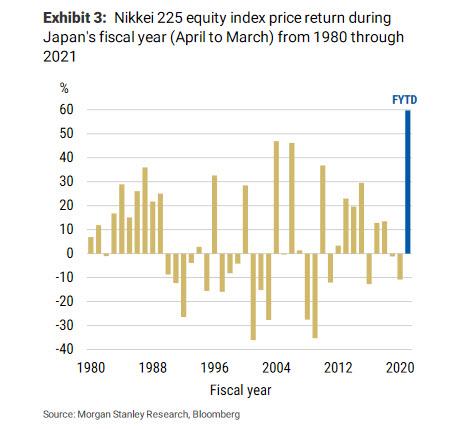

According to Morgan Stanley, Japanese commercial banks hold a large number of equity shares, and the Nikkei 225 equity index put in its best fiscal year performance in decades. In other words, for the commercial banks, the income from bond holdings wasn't necessary to make the year a successful one. Consider it one massive pension rebalance ahead of the March 31 fiscal year end... only this one was among commercial banks.

In addition, Hornbach adds that it was no longer necessary to take the risk that bond yields would keep rising, thereby subjecting their bond portfolios to capital losses in the last quarter of their fiscal year. At the same time, with a new fiscal year comes new revenue targets. And unless the banks have confidence in the Nikkei 225 index continuing to rise, the much more attractive carry and expected rolldown in the Treasury market will seem very appealing, according to the Morgan Stanley strategist.

In addition, the ability to realize that expected rolldown has been greatly enhanced by the higher bar the Fed set for tapering asset purchases and hiking rates.

简介: 日本持续的年终抛售导致了全球范围内不利的多米诺骨牌效应,最终引发了全球债券和股票市场的动荡。但是,现在已经过去了,一旦会计年度结束,日本银行将再次开始购买大量美国TSY。尽管下周股票将在哪里交易还有待观察(请参阅“月底设定的强制性养老金出售与量化购买之间的史诗冲突)”),现在看来第二季度将开始爆炸,因为在收益率下滑和刺激性检查之间,标准普尔指数最终将升至神话4,000水平之上。

泰勒·德登(Tyler Durden) 周二,03/23/2021-18:55